Research Report: 2011 Cloud Computing Predictions For Vendors And Solution Providers

This blog was jointly posted by @Chirag_Mehta (Independent Blogger On Cloud Computing) and @rwang0 (Principal Analyst and CEO, Constellation Research, Inc.)

Part 1 was featured on Forbes: 2011 Cloud Computing Predictions For CIO’s And Business Technology Leaders

As Cloud Leaders Widen The Gap, Legacy Vendors Attempt A Fast Follow

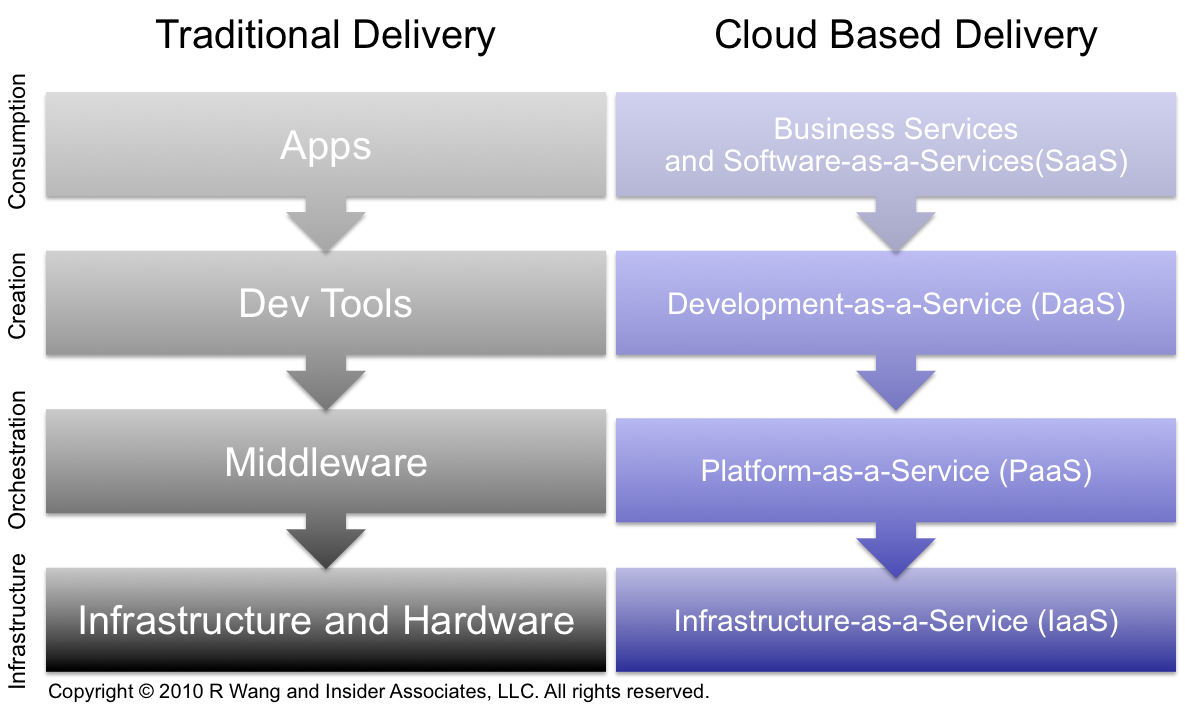

Cloud computing leaders have innovated with rapid development cycles, true elasticity, pay as you go pricing models, try before buy marketing, and growing developer ecosystems. Once dismissed as a minor blip and nuisance to the legacy incumbents, those vendors who scoffed cloud leaders now must quickly catch up across each of the four layers of cloud computing (i.e. consumption, creation, orchestration, and infrastructure) or face peril in both revenues and mindshare (see Figure 1). 2010 saw an about face from most vendors dipping their toe into the inevitable. As vendors lay on the full marketing push behind cloud in 2011, customers can expect that:

Figure 1. The Four Layers Of Cloud Computing

General Trends

- Leading cloud incumbents will diversify into adjacencies. The incumbents, mainly through acquisitions, will diversify into adjacencies as part of an effort to expand their cloud portfolio. This will result into blurry boundaries between the cloud, storage virtualization, data centers, and network virtualization. Cloud vendors will seek tighter partnerships across the 4 layers of cloud computing as a benefit to customers. One side benefit - partnerships serve as a pre-cursor to mergers and as a defensive position against legacy on-premises mega vendors playing catch up.

- Cloud vendors will focus on the global cloud. The cloud vendors who initially started with the North America and followed the European market, will now likely to expand in Asia and Latin America. Some regions such as Brazil, Poland, China, Japan, and India will spawn regional cloud providers. The result - accelerated cloud adoption in those countries, who resisted to use a non-local cloud provider. Cloud will prove to be popular in countries where software piracy has proven to be an issue.

- Legacy vendors without true Cloud architectures will continue to cloud wash with marketing FUD. Vendors who lack the key elements of cloud computing will continue to confuse the market with co-opted messages on private cloud, multi-instance, virtualization, and point to point integration until they have acquired or built the optimal cloud technologies. Expect more old wine (and vinegar, not balsamic but the real sour kind, in some cases) in new bottles: The legacy vendors will re-define what cloud means based on what they can package based on their existing efforts without re-thinking the end-to-end architecture and product portfolio from grounds-up.

- Tech vendors will make the shift to Information Brokers. SaaS and Cloud deployments provide companies with hidden value and software companies with new revenues streams. Data will become more valuable than the software code. Three future profit pools willl include benchmarking, trending, and prediction. The market impact - new service based sub-categories such as data-as-service and analysis-as-a-service will drive information brokering and future BPO models.

SaaS (Consumption Layer)

- Everyone will take the SaaS offensive. Every hardware and system integrator seeking higher profit margins will join the Cloud party for the higher margins. Software is the key to future revenue growth and a cloud offense ensures the highest degree of success and lowest risk factors. Hardware vendors will continue to acquire key integration, storage, and management assets. System integrators will begin by betting on a few platforms, eventually realizing they need to own their own stack or face a replay of the past stack wars.

- On-premise enterprise ISVs will push for a private cloud. The on-premise enterprise ISVs are struggling to keep up with the on-premise license revenue and are not yet ready to move to SaaS because of margin cannibalization fears,lack of scalable platforms, and a dirth of experience to run a SaaS business from a sales and operation perspectives. These on-premise enterprise software vendors will make a final push for an on-premise cloud that would mimic the behavior of a private cloud. Unfortunately, this will essentially be a packaging exercise to sell more on-premise software. This flavor of cloud will promise the cloud benefits delivered to a customer's door such as pre-configured settings, improved lifecycle, and black-box appliance. These are not cloud applications but will be sold and marketed as such.

- Money and margin will come from verticalized cloud apps. Last mile solutions continue to be a key area of focus. Those providers with business process expertise gain new channels to monetize vertical knowledge. Expect an explosion of vertical apps by end of 2011. More importantly, as the buying power shifts away from the IT towards the lines of businesses, highly verticalized solutions solving specific niche problems will have the greatest opportunities for market success.

- Many legacy vendors might not make the transition to cloud and will be left behind. Few vendors, especially the legacy public ones, lack the financial where with all and investor stomachs to weather declining profit margins and lower average sales prices. In addition, most vendors will not have the credibility to to shift and migrate existing users to newer platforms. Legacy customers will most likely not migrate to new SaaS offerings due to lack of parity in functionality and inability to migrate existing customizations.

- Social cloud emerges as a key component platform. The mature SaaS vendors that have optimized their "cloud before the cloud" platform, will likely add the social domain on top of their existing solutions to leverage the existing customer base and network effects. Expect to see some shake-out in the social CRM category. A few existing SCRM vendors will deliver more and more solutions from the cloud and will further invest into their platforms to make it scalable, multi-tenant, and economically viable. Vendors can expect to see some more VC investment, a possible IPO, and consolidation across all the sales channels.

DaaS & Paas (Creation and Orchestration Layers)

- Battle for PaaS begins with developers. Winning the hearts and minds will drive the key goals of PaaS providers. As mobile, social, and cloud intersect, expect new battle lines to be drawn by existing vendors seeking entry in the cloud. The first platform to enable write once deploy any how will win. PaaS vendors will seek to incorporate the latest disruptive technologies in order to attract the right class of developers and drive continuous innovation into the platform.

- Vendors must own the platform (both DaaS and Saas) to survive. ISV’s who give up on investing in their own cloud platform to other ISV’s will be relegated to second class citizens. Despite the tremendous upfront cost savings, these platform moves cut-off future revenue streams as the stack wars move to the cloud. For example, ISV’s will avoid Java to mitigate risk with Oracle or IBM. The ability to control information brokering services will be limited to the platform owner.

- Tension between indirect channel partners and vendors in the cloud will only increase. Cloud shifts customer account control to the vendor. Partners who wholeheartedly embrace the cloud risk losing direct relationships with their customers. In the case of .NET development in Azure, greater allegiance by partners to Microsoft will result in less account control with Azure.

- PaaS will be modularized and niche. New PaaS vendors will focus on delivering specific modules to compete with end-to-end application platforms. One approach - dominate niche areas int the cloud such as programming language runtimes, social media proxies, algorithmic SDK, etc. Expect more players to jump into fill big gaps in big data, predictive analytics and information management.

- Mobile app development will move to the cloud. App dev professionals and developers want one place to reach the mobile enterprise to build, mange, and deliver. The app dev life cycles will follow the delivery models and device management will prove to be the keystone in ensuring the complete development experience. Vendors should expect the cloud to be the predominant delivery channel for mobile apps to end users. Success will require seamless management of extensions and disconnected support.

IaaS (Infrastructure Layer)

- Cloud management will continue to grow and consolidate. Cloud management tools saw significant growth and investment in the last couple of years. This trend will continue. Expect to see a lot more investment in this category as increasing customer adoption drives demand for tools to manage hybrid landscapes. Also expect consolidation in this category as several VC-backed start-ups seek profitable and graceful exits.

- Cloud storage will be a hot cake. Explosive growths in information in many verticals for early adopters already factor into this fast-growing category. With more and more data moving to the cloud, customers can anticipate significant innovation in this category including SSD-based block storage, replication, security, alternate file systems, etc. Data-as-a-service and NoSQL PaaS category will further boost the growth.

- NoSQL will skyrocket in market share and acceptance. Substantial growth in the number of NoSQL companies reflect an emerging trend to dump the infrastructure of SQL for non-transactional applications. The cloud inherently makes a great platform for NoSQL and that further drives the growth for data-as-a-service and storage on the cloud.

The Bottom Line For Vendors (Sell Side)

Cloud ushers a new era of computing that will displace the existing legacy vendor hegemony. Many vendors caught off guard by the shift in both technology and user sentiment must quickly make strategic course corrections of face extinction. Here are some recommendations for vendors making the shift to Cloud:

- Embrace, don't wait, don’t even hesitate. Which is worse; cannibalizing your margins or not having margins to cannibalize? Faster time to market and greater customer satisfaction will pay off. The move to cloud ensures a seat at the table for the next generation of computing.

- Begin all new development projects in the cloud. The rapid development cycles for cloud projects ensures that innovation will meet today’s time to market standards. Test out new projects in the cloud and experience rapid provisioning and elasticity. However, don’t forget to fail fast and recover quickly.

- Avoid investing in platform led apps. Apps should drive platform design not the other way around. Form really does follow function in the Cloud. Platform designs must focus on agility and scale. Apps prove out what’s really needed versus what’s theoretical. Plan for social, mobile, analytics, collaboration, and unified communications but deliver only when it makes business sense.

- Focus on developers, developers, and developers. Steve Ballmer is right. Success in the cloud will require bringing the developers with along on the PaaS journey. Don't make them wait until the platform is done. Otherwise, it may be too late for the company and developer ecosystem.

- Prioritize power usage effectiveness (PUEs). As with the factories during the last turn of century, IaaS will be the heart of delivery. Companies with the lowest cost of computing will win and be able to pass cost savings onto their customers or pocket the margin. Further, data center efficiencies do their part in green tech initiatives.

- Help customers simplify their landscape. Build compelling business cases to shift from legacy infrastructure to cloud efficiencies. Lead the race to optimize legacy at your competitor’s expense.

Your POV

What's your cloud strategy for customers in 2011? Will you make the key investments? How will you compete effectively? Looking for additional cloud strategy resources?

- Assessing SaaS and cloud options

- Evaluating Cloud integration strategies

- Designing a next gen apps strategy with cloud in mind

- Providing contract negotiations and software licensing support

- Demystifying software licensing

- Assisting with legacy ERP migration

- Planning upgrades and migration

- Performing vendor selection

- Renegotiating maintenance

Related resources and link

- News Analysis: Salesforce.com Buys Heroku For $212M – Shows Commitment To Next Gen Apps

- Event Report: PDC10 Focuses Developers On Cloud And Devices Opportunity

- Tuesday’s Tip: Customers Seek Turnkey Applications From Their Technology Provider

- Polls And Surveys: Insider Insights™ – Customer Centric Cloud Agreements

- Tuesday’s Tip: 10 SaaS/Cloud Strategies For Legacy Apps Environments

- Tuesday’s Tip: Understanding The Many Flavors of Cloud Computing and SaaS

- Research Report: The Upcoming Battle For The Largest Share Of The Tech Budget (Part 2) – Cloud Computing

- Event Report: Microsoft Worldwide Partner Conference 2010

- News Analysis: Infor’s Cloud Strategy Goes Azure With Infor24

- Research Report: The Upcoming Battle For The Largest Share Of The Tech Budget (Part 1) – Overview

- Research Report: Microsoft Partners – Before Adopting Azure, Understand the 12 Benefits And Risks

- Research Report: How SaaS Adoption Trends Show New Shifts In Technology Purchasing Power

- Event Report: Top 10 Questions To Ask At The Microsoft TechEd/STB Analyst Summit

Reprints

Reprints can be purchased through the Software Insider brand or Constellation Research, Inc. To request official reprints in PDF format, please contact [email protected].

Disclosure

Although we work closely with many mega software vendors, we want you to trust us. A full disclosure listing will be provided soon on the Constellation Research site.

Copyright © 2010 R Wang and Insider Associates, LLC. All rights reserved.